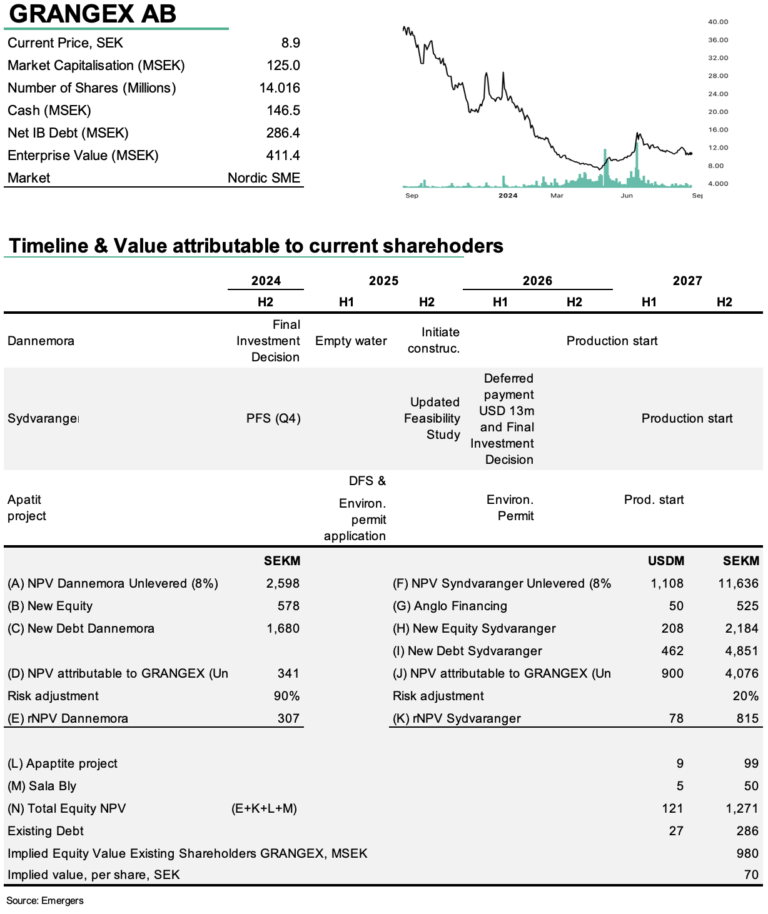

GRANGEX: Emerging as Europe’s top DR concentrate developer

With the dust settling after the acquisition of Sydvaranger and the updated DFS for Dannemora in Q2’24, the next steps for GRANGEX are now to complete a PFS (in H2’24) and DFS (mid 2025) for Sydvaranger and to complete the final project financing and investment decision for Dannemora. All in all, we see several triggers in the coming 12-24 months that should drive a revaluation of the share. Our NPV calculation includes a high degree of uncertainty, especially for Sydvaranger. However, with new insights into the balance sheet and debt following Sydvaranger’s entry into the books, we’ve made a slight adjustment to the total rNPV-based fair value for today’s equity holders, now set at SEK 70 (previously SEK 73) per share, contingent upon successfully securing financing for Dannemora during H2’24.

Strategic expansion through Sydvaranger acquisition

The acquisition of Norway’s largest and Europe’s third-largest iron ore mine, Sydvaranger in May has transformed GRANGEX into a significantly larger entity and solidified its position as the mining developer in Europe with the largest realistic short-term production potential of DR (Direct Reduction) concentrate. It has deepened GRANGEX’s collaboration with Anglo American through an off-take agreement for 70-75 million tons of high-quality concentrate over approximately 20 years. Combined with the output from Dannemora, this brings the total estimated tonnage to 81-86 million tons.

As Europe’s steel producers transition to green steelmaking, driven by the EU’s increasing carbon taxes, the demand for GRANGEX’s DR concentrate is poised to grow. Strategic goals for Sydvaranger include advancing the existing beneficiation process to produce high-quality DR concentrate, enabling the swiftest possible restart based on current infrastructure, and developing economically sustainable alternatives to minimize the existing, permitted fjord tailings deposit.

Clearer picture of the balance sheet impact of Sydvaranger

With Sydvaranger now in the books for the first time, the Q2 report shed some interesting light on the details of the deal, and the impact on the balance sheet. The royalty agreements with Anglo American are reported as a financial liability at amortized cost. Royalty payments will be made in line with the delivery and sale of iron ore during the planned production (11 years for Dannemora and 20 years for Sydvaranger), with amortization calculated per ton of ore. An accounting interest is added to the liability, with the interest continuously reported in the income statement. However, no cash flow-impacting interest payment will be made. The same applies to the deferred payment and the loan to Orion, as well as the loan to DNB, where the interest is added to the liability, allowing the company’s entire cash position of SEK 147m to be used for project development.

Set for now, but major raise on the near term horizon

The GRANGEX share has had surprising difficulty to move closer to some kind of fair value, most likely due to the uncertainties associated with future financing needs and the sheer size of the numbers. This should adjust itself somewhat as development progresses. But that depends on the company’s ability to secure financing for Dannemora during H2’24, which will be crucial for establishing investor confidence in the stock.

Key milestones for investors

As the the Sydvaranger deal has been closed and the updated DFS for Dannemora published, we now look forward to:

• Final investment decision and commencement of drainage of Dannemora in H2’24/H1’25

• PEA/PFS study on the new conditions for Sydvaranger with a higher-quality product than before

• updated DFS for Sydvaranger later in 2024

• the major capital raise slated for 2024

• Production start in Dannemora in 2026/27

• Final Investment Decision for Sydvaranger